Business

Edun, Dangiwa Resign from Tinubu’s Cabinet, Not Sacked

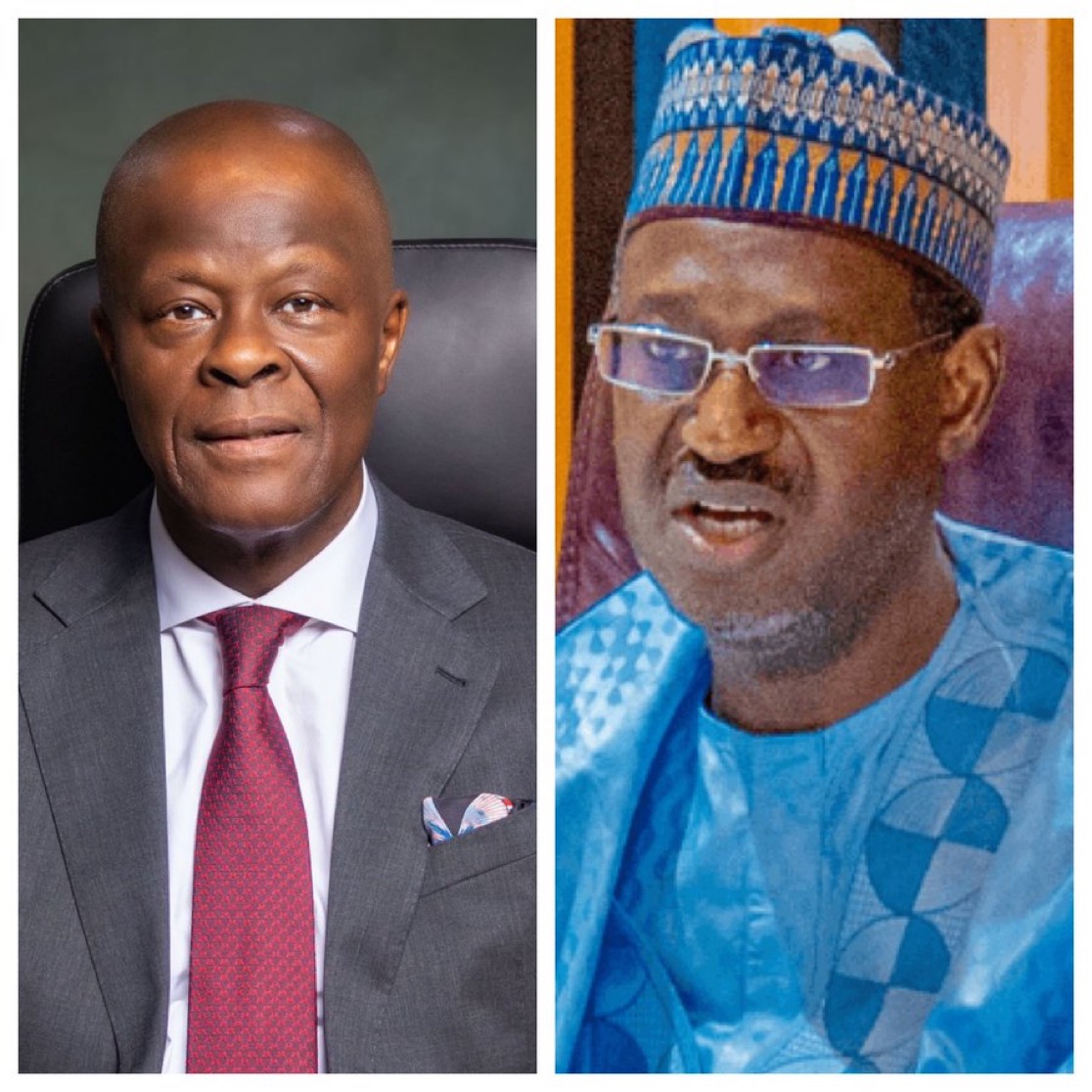

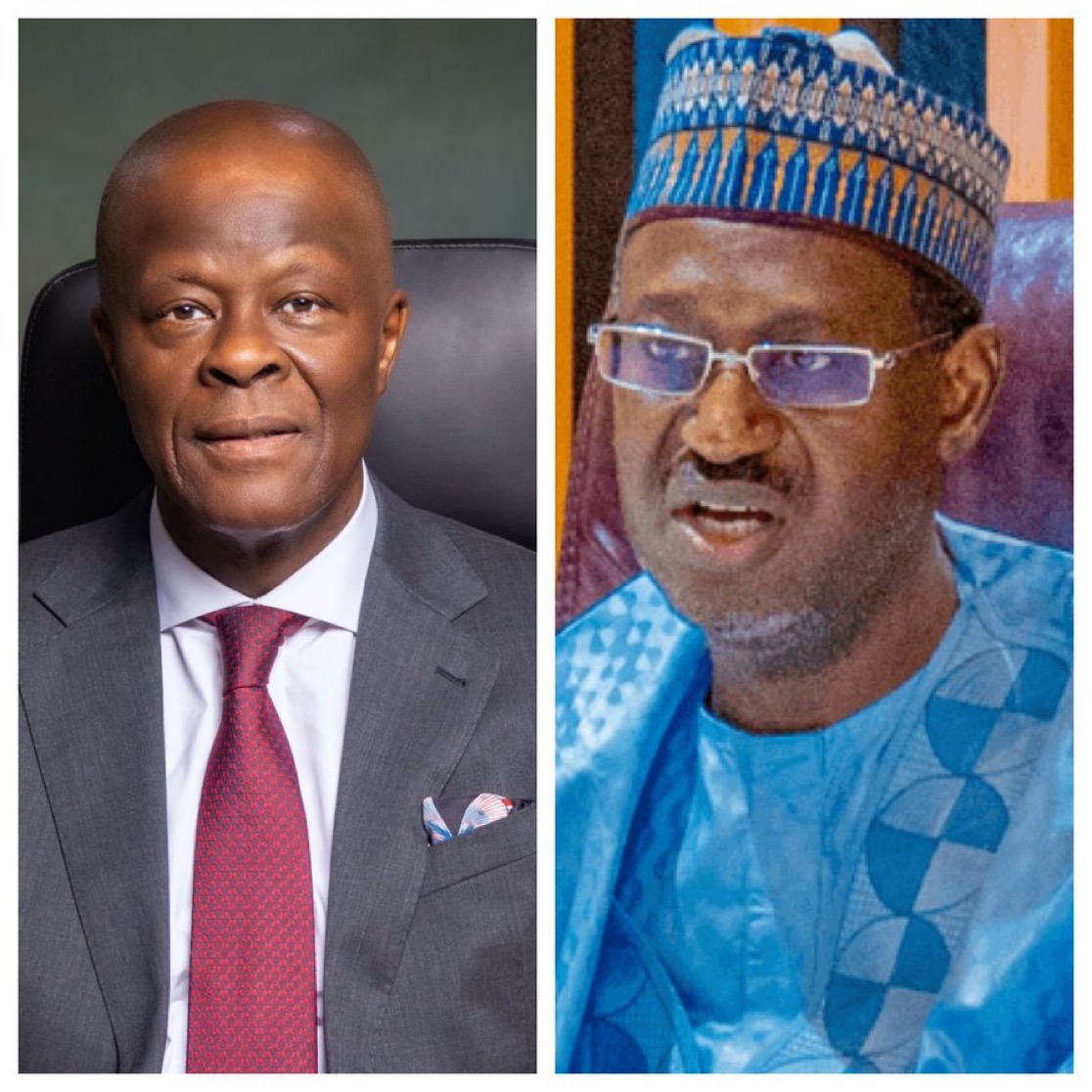

The Presidency has dismissed reports suggesting that the former Minister of Finance and Coordinating Minister of the Economy, Wale Edun, was removed from office by President Bola Ahmed Tinubu, clarifying that he voluntarily resigned on health grounds.

In a statement issued on Wednesday by the Special Adviser to the President on Information and Strategy, Bayo Onanuga, it was confirmed that Edun formally tendered his resignation before the President announced a replacement on Tuesday.

Similarly, the former Minister of Housing and Urban Development, Ahmed Musa Dangiwa, also stepped down from his position, expressing appreciation to the President for the opportunity to serve in the Federal Executive Council.

Mr. Edun, who marked his 70th birthday on Monday and has recently experienced health challenges, submitted his resignation on the same day. In his letter, he thanked the President for the opportunity to serve the nation.

“It has been an honour to be part of your administration and the Renewed Hope Agenda,” he wrote.

“Under your leadership, Nigeria has become stronger, more stable, and more respected internationally.

“I wish you continued success in the years ahead.”

Before his exit was officially announced by the Office of the Secretary to the Government of the Federation, Edun paid a farewell visit to President Tinubu at the State House on Tuesday. He later left following a private meeting that lasted about an hour, indicating his intention to focus on personal engagements.

Ahmed Musa Dangiwa, a professional architect, previously served as Managing Director of the Federal Mortgage Bank from 2015 to 2022 and as Secretary to the Katsina State Government before his appointment as minister in August 2023.

Edun, an economist and investment banker, served as Lagos State Commissioner for Finance between 1999 and 2004 during Tinubu’s tenure as governor.

He earlier worked at Chase Merchant Bank in Lagos from 1980 to 1986 before joining the World Bank under its Young Professionals Programme, where he contributed to economic and financial projects across Latin America and the Caribbean.

In 1989, he co-founded Investment Banking & Trust Company Limited (now Stanbic IBTC) and later established Denham Management Limited in 1994, which evolved into the Chapelhill Denham Group. He served as chairman of the company from 2008 to 2021.

President Tinubu has commended both Edun and Dangiwa for their service and contributions to the administration’s economic reform agenda, and wished them success in their future endeavours.

The President has also directed the newly appointed Minister of Finance, Taiwo Oyedele, to consolidate ongoing reforms and strengthen the administration’s fiscal and economic policies with renewed focus, discipline, and innovation.

In addition, President Tinubu is expected to forward the nomination of Muttaqha Rabe Darma, also from Katsina State, to the Senate for confirmation as Minister of Housing.

The post Edun, Dangiwa Resign from Tinubu’s Cabinet, Not Sacked appeared first on Business Today NG.

BY NKECHI NAECHE-ESEZOBOR—Enterprise Life Assurance (Nigeria) Limited has announced the full remittance of its statutory deposit of N1 billion to the Central Bank of Nigeria (CBN), underscoring its robust financial health and compliance with regulatory mandates.

The Managing Director and Chief Executive Officer of the company, Nelson Akerele, disclosed this during a recent media briefing while addressing the firm’s capital positioning and compliance with the National Insurance Commission (NAICOM).

According to Akerele, Enterprise Life—which entered the Nigerian market approximately five years ago alongside peers like Heirs General and Heirs Life—has progressively built on its foundational capital structure to satisfy current regulatory thresholds.

“We started with ₦8 billion,” Akerele stated, recalling the company’s entry as one of the four entities licensed in that licensing wave. “What we have as a statutory deposit right now, as I speak, is ₦1 billion, which has been fully remitted to the designated account assigned to us.”

Beyond meeting the statutory deposit mandate, the Enterprise Life boss revealed that the company has fully satisfied its Minimum Capital Requirement (MCR).

He attributed this seamless compliance to a deliberate operational strategy that favors liquid assets over heavy fixed investments.

Unlike traditional players with massive capital tied up in real estate, Enterprise Life has maintained an agile, cash-ready balance sheet.

“We are not heavy in terms of buildings and all that; our assets are held in liquid form—in cash and cash equivalents,” Akerele emphasized. “We are an extremely liquid company.”

This cash-heavy asset strategy positions the insurer to promptly meet its obligations, match underwriting risks effectively, and settle policyholders’ claims without the delays often associated with liquidating physical property.

The announcement comes at a critical time when NAICOM continues to emphasize stricter solvency and liquidity management across the Nigerian insurance ecosystem to boost public confidence in the sector.

The post Enterprise Life Assurance Meets Full Regulatory Capital Requirements, Boosts Liquidity appeared first on Business Today NG.

The National Information Technology Development Agency (NITDA) has partnered with Meta to promote responsible digital citizenship and protect young Nigerians online.

The Director-General of NITDA, Kashifu Inuwa, disclosed the partnership at the Youth Safety Summit organised by Meta on Thursday.

At the summit, held in Abuja, Meta, in partnership with NITDA and the Federal Ministry of Youth Development, also launched the Youth Online Safety Campaign and My Digital World 2.0.

The stakeholders at the summit, including government officials, civil society organisations, educators, and industry leaders, deliberated on strategies to create a safer digital environment for young people.

Represented by Ahmed Tambuwal, acting director of NITDA’s Digital Literacy and Capacity Building Department, Mr Inuwa said the agency remained committed to ensuring that young people enjoy safe, positive, and age-appropriate online experiences.

He noted that NITDA’s ongoing nationwide digital literacy programmes would receive a significant boost through its collaboration with Meta, particularly in advancing online safety education among young Nigerians.

READ ALSO: NITDA enters pact with DAWN Commission to accelerate digital literacy in Southwest

According to him, the partnership seeks to integrate online safety education into the school system, equipping students with the knowledge, skills, and values required to use digital technologies safely, responsibly, and productively.

Stakeholders at the event emphasised the need for stronger collaboration among government agencies, technology companies, educators, and civil society groups to address emerging online risks and promote digital well-being among young people.

The initiatives are expected to enhance digital literacy, strengthen online safety awareness, and support efforts to create a more secure and inclusive digital ecosystem for Nigerian youths.

-

Business4 days ago

Business4 days agoOndo Police Foil Two Kidnap Attempts in Owo, Rescue Victims and Family Members

-

Business2 days ago

Business2 days agoCement maker Lafarge Africa renamed HBM Nigeria Plc

-

News3 days ago

News3 days agoI’m Jealous Wike is in PDP – APC Chairman, Nentawe Yilwatda admits

-

Business3 days ago

Africa records hydropower growth but Nigeria still suffers power shortages — Report